Selim Raihan and Sunera Saba Khan

The Bangladesh economy over the past two and half decades has been experiencing steady rise in economic growth rate which has been accompanied by country’s increasing trade-GDP ratio. The economy has become more and more trade-oriented. However, when it comes to integrating with its neighboring countries, there are still large untapped potentials for Bangladesh to gain from such integration. Effective regional integration, through enhanced scope for larger economies of scale and pathway for integration with global and regional value chains, can be a critical tool for Bangladesh to boost its economic growth process. Over the past three decades, regional integration agenda for Bangladesh has focused primarily on integrating with its South Asian neighboring countries. However, there are reasons to believe that Bangladesh can also gain significantly by integrating more with the East Asian countries (China, Japan and South Korea) and Southeast Asian countries (10 ASEAN countries. i.e. Brunei, Myanmar, Cambodia, Indonesia, Laos, Malaysia, the Philippines, Singapore, Thailand and Vietnam). Bangladesh government also wants to pursue the “Look East Policy”, and for this it is high time for Bangladesh to begin the quest for expanded trade and investment opportunities with these countries.

The Bangladesh economy is now at a cross-road. Further growth acceleration is essential to make a transition to a higher growth path in order to obtain the upper-middle income country status. The country needs to promote economic diversification, with a simultaneous diversification of the export basket, in order to boost its growth rate. When it comes to export diversification, in terms of both product and destination, integration with East and Southeast Asian countries is very important for Bangladesh. A major reason why integration with East and Southeast Asia will prove to be beneficial for Bangladesh is because East and Southeast Asia are essentially integrated with the Global Value Chains (GVCs) in a number of manufacturing products. Thus, such integration will pave the way for linking Bangladesh with wider GVCs and in diversifying its export basket. In addition, flows of Foreign Direct Investment (FDI) from these countries to Bangladesh will be beneficial for the economy. Among the Southeast Asian countries Indonesia, Malaysia and Vietnam are large exporters of electronics, machinery and leather goods, primarily driven by the leading multinational companies in the world. Therefore, integration will lead to a number of multinational companies specialized in electronics, machinery and leather goods investing in Bangladesh, thus generating large spill-over benefits to the domestic economy.

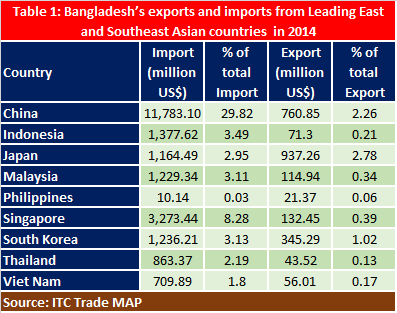

However, Bangladesh’s level of integration with East and Southeast Asian countries is mixed. Table 1 clearly depicts that Bangladesh’s imports from East and Southeast Asia are significantly higher compared to exports to these regions. With a share of around 30% of total import, China in 2014 was the major source of import for Bangladesh. Singapore also had more than 8% share. Except Philippines, Thailand and Vietnam, all other countries accounted for more than 1 billion US$ import for Bangladesh. In contrast, Bangladesh’s exports to most of these countries were very low. The largest export was to Japan, which was close to 1 billion US$, followed by export to China by 760 million US$. The lowest export was to the Philippines with an amount of only 21.4 million US$.

The current scenario clearly portrays that Bangladesh’s exports to East and Southeast Asia are significantly low and immediate initiatives need to be adopted in order to raise export levels. Product diversification followed by market and need assessments in those countries will help Bangladesh accelerate the desired integration process. Bangladesh’s exports to these countries can be improved if Bangladesh engages in exports of non-traditional goods. Bangladesh should actively pursue the agenda of free trade agreements (FTAs) with these countries, either bilaterally or with the region as a whole (i.e. with ASEAN). In this context, it is important to mention that four Southeast Asian countries (Brunei Darussalam, Malaysia, Singapore and Vietnam) are part of the recently signed Trans-Pacific Partnership Agreement (TPP), which is a free trade agreement among nine countries. The other countries are the United States, Australia, Chile, New Zealand and Peru. Furthermore, all 10 ASEAN countries are part of the proposed Regional Comprehensive Economic Partnership (RCEP), which is a free trade agreement (FTA) between these ten countries and the six states with which ASEAN has existing FTAs (Australia, China, India, Japan, South Korea and New Zealand). With the emergence of these mega FTAs, where a large number of East and Southeast Asian countries are involved, there are risks of negative impacts on Bangladesh as Bangladesh is not part of these FTAs. Therefore, it is imperative for Bangladesh to proactively take up the FTA agenda with the East and Southeast Asian countries. At this moment, Bangladesh is part of BIMSTEC, where two of the Southeast Asian countries (Thailand and Myanmar) are members. However, the BIMSTEC FTA is yet to be implemented.

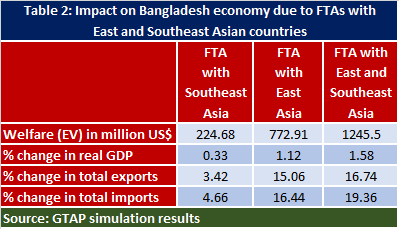

Table 2 presents the results from simulations using the GTAP model, where we have explored hypothetical scenarios of FTAs between Bangladesh and East and Southeast Asian countries. Under certain assumptions, Bangladesh stands to gain from these FTAs. The largest gain seems to appear from the FTA with both East and Southeast Asian countries.

As far as Bangladesh’s imports from these countries are concerned a major chunk of the imports are used as raw materials and capital machineries in the export industry as well as in the domestic industrial sector. Being the dominant export sector, until now the benefits from such imports have largely been enjoyed by the RMG sector in Bangladesh. However, the non-RMG export sectors and domestic manufacturing sectors have not been able to benefit much from such imports. In addition, there are a number of policy-induced and supply-side constraints for these non-RMG sectors which constrict their expansion. Sector specific infrastructural problems, poor overall physical infrastructure, lack of investment fund and working capital, high interest rate, shortage of skilled workers, invisible costs of doing business, etc. are major impediments to export prospects and export diversification. Therefore, while pursuing the deeper integration agenda, it is also imperative to address these supply side constraints; otherwise the country will not be able to make much progress towards export diversification and will fail to reap the benefit from such integration.

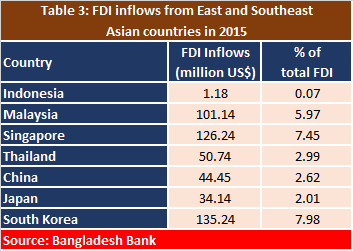

Bangladesh should also invite much larger FDIs from East and Southeast Asian countries. The current level of total FDI in Bangladesh is very low, and Table 3 shows that FDI inflows from East and Southeast Asia are also low. Bangladesh can immensely benefit from higher FDI inflows from these countries in terms of export diversification and large employment generation. The government’s initiative of setting up special economic zones should give priorities to the leading investors from East and Southeast Asian countries targeting electronics, leather and different processing industries. Finally, enhanced connectivity with China and other Southeast Asian countries through BCIM, Asian highway and Trans-Asian Railway network should be accentuated.